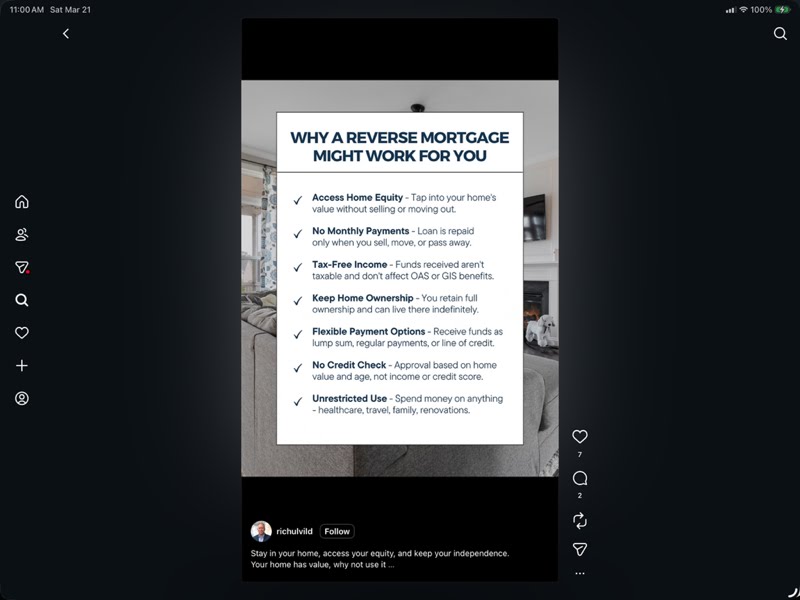

01

DSCR · EXAMPLE 1 of 13

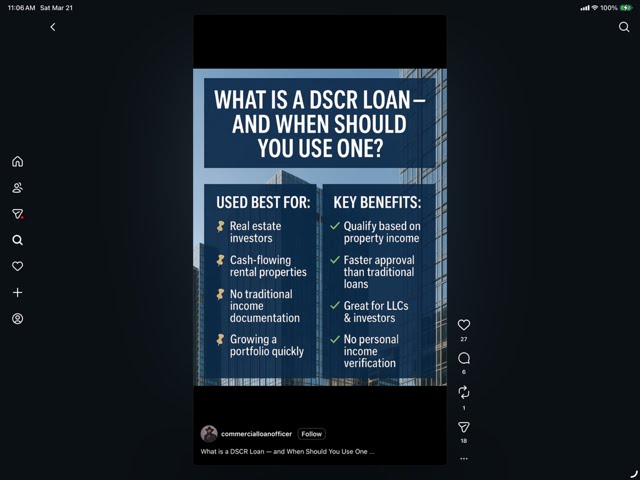

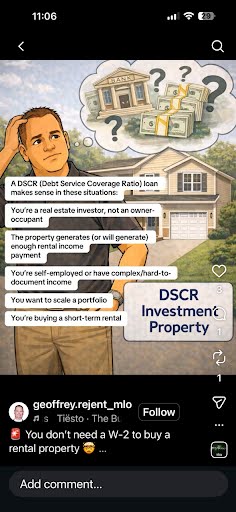

(no H1; first body line) A DSCR (Debt Service Coverage Ratio) loan makes sense in these situations:

Source: geoffrey.rejent_mlo

①②③④

①②③④

Composition

- Layout: side-by-side (illustrated portrait left + thought-bubble right)

- Logo placement: none (creator handle in IG chrome only)

- Visual flow: vertical stack of bullet pills with portrait anchor

- White space: dense

Numbered elements

- ① portrait illustration of male professional

- ② thought-bubble with bank/cash/houses + question marks

- ③ teal callout pill 'DSCR Investment Property'

- ④ stacked white text-block bullets listing 6 borrower-fit situations

Style

- Treatment: illustrated

- Photography: n/a (vector portrait)

- Typography: sans-serif

- Mood: educational / explanatory / approachable

- Palette:

Messaging (verbatim)

| H1 | (no H1; first body line) A DSCR (Debt Service Coverage Ratio) loan makes sense in these situations: |

| Subhead | — |

| Body | You're a real estate investor, not an owner-occupant / The property generates (or will generate) enough rental income payment / You're self-employed or have complex/hard-to-document income / You want to scale a portfolio / You're buying a short-term rental |

| CTA button | (none — caption emoji 'You don't need a W-2 to buy a rental property') |

| Brand lockup | (creator handle only) |

| Compliance | (none visible) |

Strengths

Bullet-list pattern is highly scannable; defines DSCR jargon parenthetically (lowers reader threshold); caption hook 'no W-2' is sharp.

Weaknesses

No brand lockup, no NMLS, no CTA button. Illustration is generic stock-style. No headline hierarchy — eyes wander.

⚠ Compliance Audit · Example 01

VIOLATIONViolations · 4

SAFE Act 12 USC §5103(3) + Reg H 12 CFR §1008.103(e)(7)

No individual MLO NMLS # visible on creative

Est. range: $1,000 – $10,000

· Mid estimate: $5,500

SAFE Act + Reg H

No corporate NMLS # disclosed

Est. range: $1,000 – $10,000

· Mid estimate: $5,500

Fair Housing Act 42 USC §3604(c) + 24 CFR Part 109

No Equal Housing Lender mark on residential investment-property lending creative

Est. range: $16,000 – $100,000

· Mid estimate: $16,000

CFPB UDAAP

Generic illustration + no brand lockup ambiguates the responsible advertiser — deceptive omission risk

Est. range: $5,000 – $50,000

· Mid estimate: $10,000

Disclaimers present: NONE

Responsible parties (regulatory exposure):

- Individual MLO (geoffrey.rejent_mlo)

- Brokerage of record

Total estimated exposure for this image:

$37,000

range $23,000 – $170,000